Education planning has serious financial consequences

Article Licenses: CA, unknown, unknown

Advisor Licenses:

Compliant content provided by Adviceon® Media for educational purposes only.

As parents, we need to consider the effect that education will have on the future income and lifestyle of our children. When Steve Jobs of Apple knew he had a short time to live, he became assertively interested and vowed that he would do everything in his power to ensure that his son received a good education.

As the Internet brings many changes quickly, we are seeing many manufacturers moving plants overseas. Stephen Covey, the best-selling author of The 7 Habits of Highly Effective People, predicted a need for technological education several years ago, echoing what we see everywhere: manufacturing increasingly calls for brain work rather than metal-bashing that empower the industrial age — further making a point:

The winds of education reform are beginning to stir once again. Our collective conscience is being nudged. And there’s a good reason. The world has moved into one of the most profound eras of change in human history. Our children, for the most part, are just not prepared for the new reality. The gap is widening. And we know it.

Parents see the chaos, the economic uncertainty, the stress and the complexity in the world, and know deep down that the traditional three “R’s” — reading, writing, and arithmetic — are necessary, but not enough.

Today robotics and artificial intelligence call for another education revolution. This time, however, simply cramming more schooling in at the start is not enough. People must also be able to acquire new skills throughout their careers.

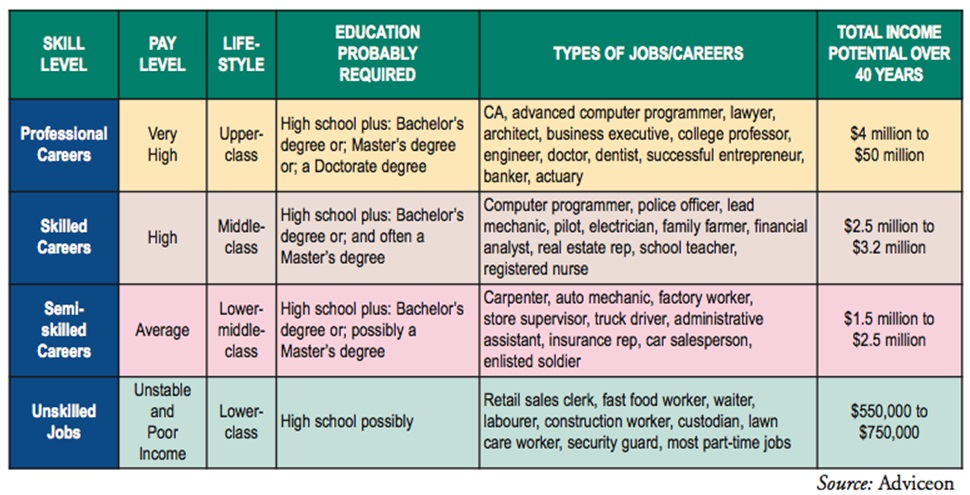

The following grid estimates the effect of educational decision-making on a child’s education. Income and future lifestyle can be severely affected by poor choices. When a child has the capacity and talent for a higher level of educational goal-setting and achievement, this needs to be developed appropriately.

What ways can we plan for our Child’s education? Consider using both the traditional Registered Educational Savings Plan (RESP) and the Tax-Free Savings Account (TFSA) as an educational savings vehicle. A TFSA offers parents another tax-efficient method to provide for education planning.

Using the TFSA for Educational Planning

Canadian residents age 18 or older can contribute up to a TFSA.

TFSA Contribution Limits

- 2009 to 2012: $5,000

- 2013 and 2014: $5,500

- 2015: $10,000

- 2016 to 2018: $5,500

- 2019 to 2022: $6,000

- 2023: $6,500

- 2024: $7,000

Contributions are not deductible from your taxable income. You can add any unused contributions of your annual limit, cumulative back to 2009.

Using the RESP for Educational Planning

- You can save for a child’s education using the RESP. The Government of Canada will also help you save money through the Canada Education Savings Grant (CESG).

- Your advisor can help you understand what RESP options is available to you in your province.

The Advisor and Manulife Securities Incorporated, ("Manulife Securities") do not make

any representation that the information in any linked site is accurate and

will not accept any responsibility or liability for any inaccuracies in

the information not maintained by them, such as linked sites. Any opinion

or advice expressed in a linked site should not be construed as the opinion

or advice of the advisor or Manulife Securities. The information in this

communication is subject to change without notice.

This publication contains opinions of the writer and may not reflect opinions

of the Advisor and Manulife Securities Incorporated, the information contained

herein was obtained from sources believed to be reliable, no representation,

or warranty, express or implied, is made by the writer, Manulife Securities or

any other person as to its accuracy, completeness or correctness. This

publication is not an offer to sell or a solicitation of an offer to buy any

of the securities. The securities discussed in this publication may not be

eligible for sale in some jurisdictions. If you are not a Canadian resident,

this report should not have been delivered to you. This publication is not

meant to provide legal or account advice. As each situation is different you

should consult your own professional Advisors for advice based on your

specific circumstances.